HOW TO SELECT THE RIGHT MORTGAGE

INTRODUCTION

As you start to consider your mortgage options, you may quickly find yourself overwhelmed by the sheer number of choices. Give the number of bells and whistles that most mortgages can come with, the number or possible combinations means that literally hundreds of choices available.

Talk about mortgage migraine!

There are three questions you need to ask yourself to help you pick the right mortgage:

- How long do you plan to keep your mortgage in place?

- How much financial risk can you accept?

- How much money do you need to borrow?

HOW LONG DO YOU PLAN TO KEEP YOUR HOME?

Many home buyers don’t expect to stay in their current homes for a long period of time. If a person intends to keep a residence for 5 years or less, you should consider an adjustable-rate mortgage (ARM) and/or a “No Point” mortgage (no discount or origination points).

Why an ARM? Because and ARM guarantees a rate for a short period of time, there’s less risk to the lender. As a result, the starting rate is lower than a fixed rate loan.

A mortgage lender takes more risk when lending money at a fixed rate of interest for a long period of time. Thus, compared with an ARM, where the lender is committing to the initial interest rate for a relatively short period of time, lenders charge a premium interest rate for a fixed-rate loan.

The interest rates used to determine most ARMs are short-term interest rates, whereas long-term interest rates dictate the terms of fixed-rate mortgages. During most time periods, longer-term rates are higher because of the greater risk the lender accepts in committing to a longer-term rate.

The down side to an ARM, however, is that if interest rates rise, you may find yourself paying more interest in future years than you would be paying had you taken out a fixed-rate loan from the get-go. If you’re reasonably certain you’ll hold onto your home for five or fewer years, you should come out ahead with an adjustable.

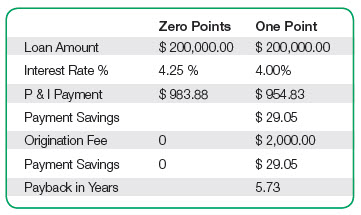

Why a No Point Mortgage? If you are not comfortable accepting the risk associated with an ARM but still do not expect to keep your mortgage in place for more than 5 to 7 years, then a fixed rate loan with reduced fees makes more sense. This is accomplished by accepting a higher than market rate with reduced fees. As the chart below shows, the break-even point for accepting an increased of .25% in rate is less than 6 years. So, for example, if you sold your home in 4 years you would save $603.

HOW MUCH FINANCIAL RISK CAN YOU ACCEPT?

Many homebuyers, particularly first-timers, take an adjustable-rate mortgage (ARM) because doing so allows them to stretch and buy a more expensive home. We Americans are not known for our delayed gratification discipline!

If you’re considering an ARM, you must understand what rising interest rates and a rising monthly mortgage payment could do to your personal finances. Only consider taking an ARM if you can answer “yes” to all of the following questions:

- Is your monthly budget such that you can afford higher mortgage payments later on and still accomplish other financial goals?

- Do you have an emergency reserve, equal to at least three to six months of living expenses, that you can tap into to make higher monthly mortgage payments?

- Can you afford the highest payment allowed on the adjustable-rate mortgage?

- Can you handle the psychological stress of changing interest rates and mortgage payments?

If you are fiscally positioned to take on the financial risks inherent to an ARM, by all means consider one. Even if interest rates do rise, as they inevitably and eventually will, they will come back down. If you can stick with your ARM through times of high and low interest rates, you are still likely to come out ahead.

HOW MUCH MONEY DO YOU NEED TO BORROW?

One factor that distinguishes the best mortgage from an inferior loan is that the best mortgage is the best deal you can get. Why waste your hard-earned money on the second-best mortgage? The amount of money you borrow can greatly affect your interest rate. You need to carefully consider how much money you need to borrow.

Conventional mortgages that stay within Fannie Mae and Freddie Mac loan limits established each year by Congress are called conforming loans. Mortgages that exceed the maximum permissible loan amounts are referred to either as nonconforming loans or jumbo loans. Mortgage interest rates for conforming loans typically run 0.25 percent to 0.50 percent lower. Keeping the amount of money you borrow under that all-important loan limit will save you big bucks over the life of your loan.

If your mortgage slightly surpasses Fannie Mae and Freddie Mac’s loan limit, here are two ways to bring it into conformity:

- Buy a less expensive home.

- Increase your down payment to reduce the mortgage.

In conclusion, there are many mortgage options people can use to save money and live within their financial means.

We can refer you to a licensed mortgage professional to help you understand your options and make the right mortgage decisions.

Tags: mortgage