Higher mortgage rates, along with elevated sales prices and a lack of housing inventory, have continued to impact market activity during the summer homebuying season. The average 30-year fixed-rate mortgage has remained above 6.5% since May, recently hitting a two-decade high in August, according to Freddie Mac. As a result, existing-home sales have

continued to slow nationwide, dropping 2.2% month-over-month as of last measure, with sales down 16.6% compared to the same time last year, according to the National Association of REALTORS® (NAR).

New Listings decreased 23.5 percent for Single Family and 30.1 percent for Townhouse/Condo. Pending Sales decreased 1.7 percent for Single Family and 17.2 percent for Townhouse/Condo. Inventory decreased 28.4 percent for Single Family and 38.9 percent for Townhouse/Condo.

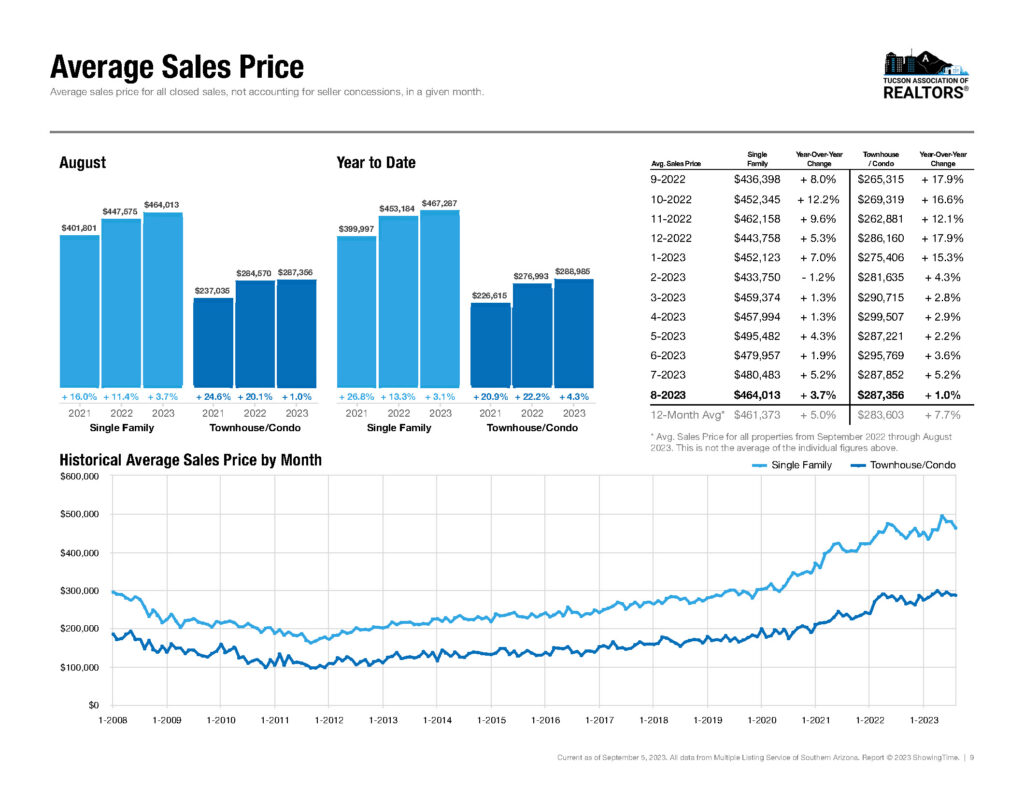

Median Sales Price increased 2.9 percent to $385,000 for Single Family and 1.0 percent to $264,900 for Townhouse/Condo. Days on Market increased 54.5 percent for Single Family and 61.1 percent for Townhouse/Condo. Months Supply of Inventory decreased 5.0 percent for Single Family and 21.4 percent for Townhouse/Condo.

Falling home sales have done little to cool home prices, however, which have continued to sit at record high levels nationally thanks to a limited supply of homes for sale. According to NAR, there were 1.11 million homes for sale heading into August, 14.6% fewer homes than the same period last year, for a 3.3 months’ supply at the current sales pace. The shortage of homes for sale has boosted competition for available properties and is driving sales prices higher, with NAR reporting a national median existing home price of $406,700, a 1.9% increase from a year earlier.