Rising inflation, soaring home prices, and increased mortgage interest rates have combined to cause a slowdown in the U.S. housing market. To help quell inflation, which reached 8.6% as of last measure in May, the Federal Reserve raised interest rates by three quarters of a percentage point in June, the largest interest rate hike since 1994. Higher prices, coupled with 30-year fixed mortgage rates approaching 6%, have exacerbated affordability challenges and rapidly cooled demand, with home sales and mortgage applications falling sharply from a year ago.

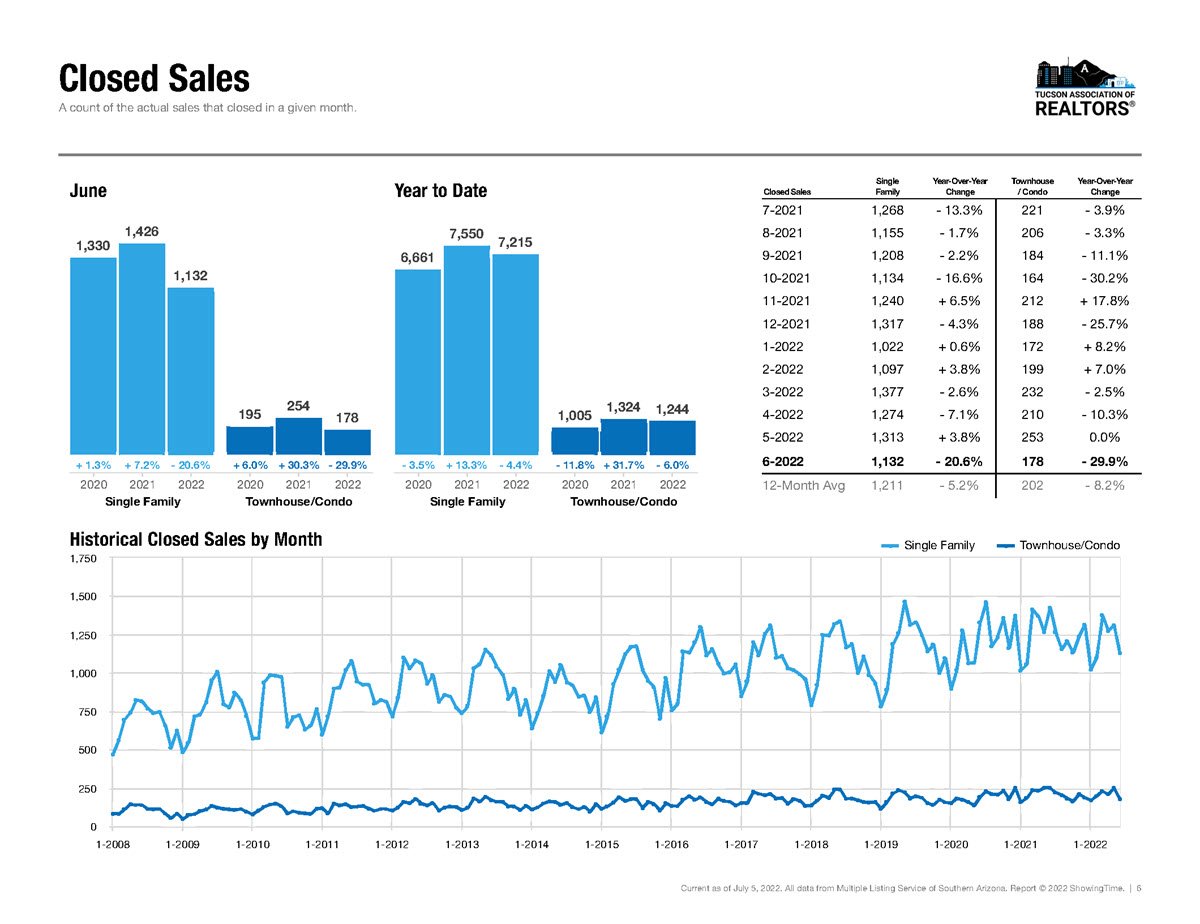

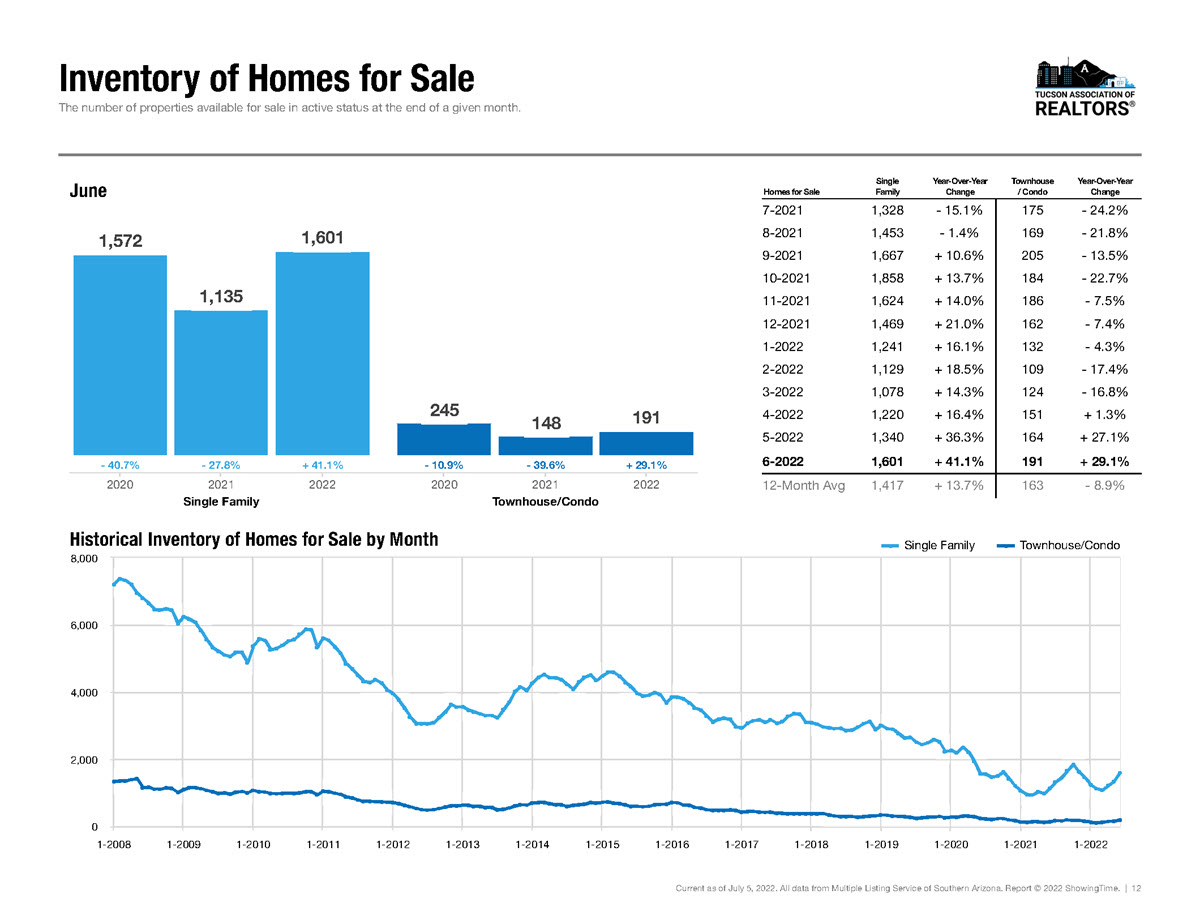

New Listings increased 4.6 percent for Single Family but decreased 1.6 percent for Townhouse/Condo. Pending Sales decreased 9.9 percent for Single Family and 8.3 percent for Townhouse/Condo. Inventory increased 41.1 percent for Single Family and 29.1 percent for Townhouse/Condo.

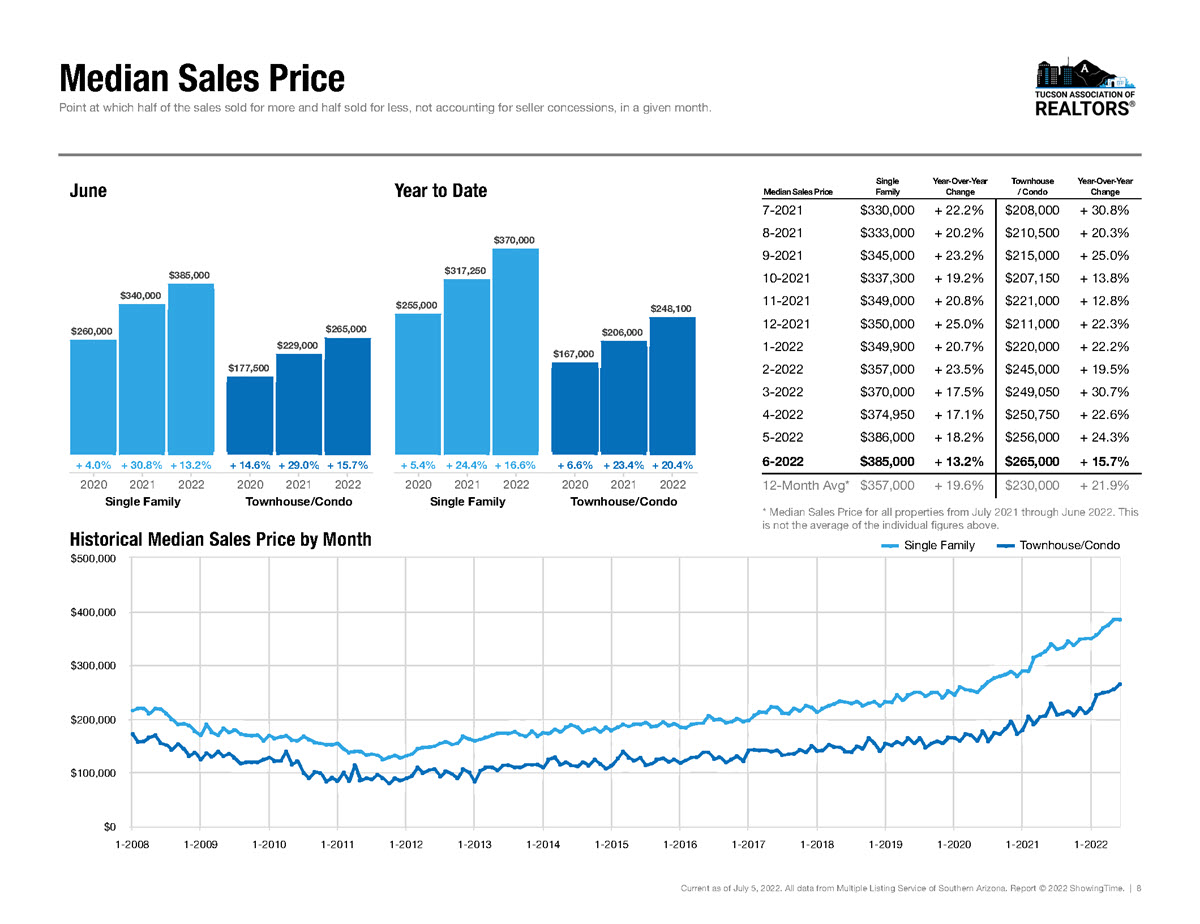

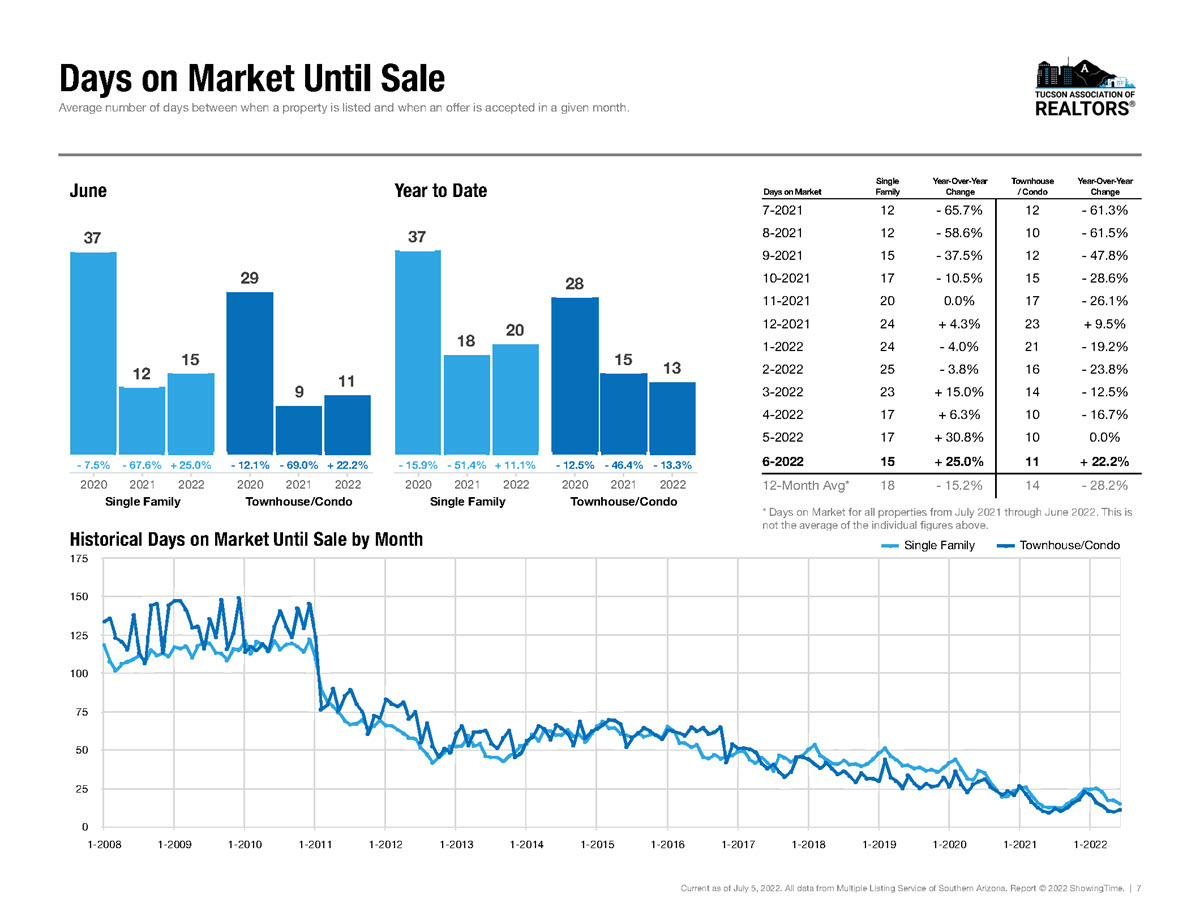

Median Sales Price increased 13.2 percent to $385,000 for Single Family and 15.7 percent to $265,000 for Townhouse/Condo. Days on Market increased 25.0 percent for Single Family and 22.2 percent for Townhouse/Condo. Months Supply of Inventory increased 44.4 percent for Single Family and 28.6 percent for Townhouse/Condo.

With monthly mortgage payments up more than 50% compared to this time

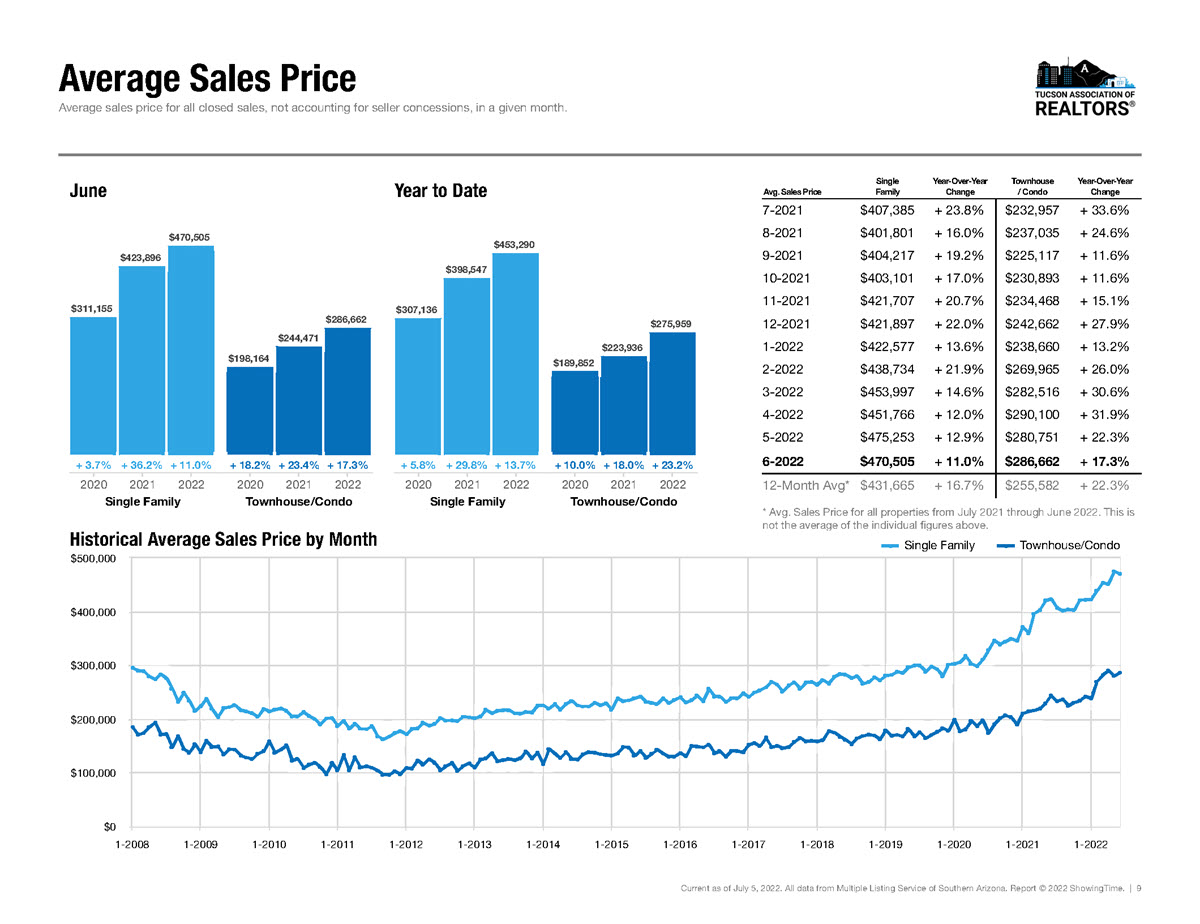

last year, the rising costs of homeownership have sidelined many prospective buyers. Nationally, the median sales price of existing homes recently exceeded $400,000 for the first time ever, a 15% increase from the same period a year ago, according to the National Association of REALTORS®. As existing home sales continue to soften nationwide, housing supply is slowly improving, with inventory up for the second straight month. In time, price growth is expected to moderate as supply grows; for now, however, inventory remains low, and buyers are feeling the squeeze of higher prices all around.